Determining the Forgiveness Amount of Your Paycheck Protection Program (PPP) Loan

Determining PPP Loan Forgiveness

Determining the Amount of Your PPP Loan

Frequently Asked Questions

The SBA has issued guidance regarding many components of the PPP calculation and forgiveness estimate, including:

Do non-partner, self-employed borrowers have different rules for calculating the amount of their PPP loan?

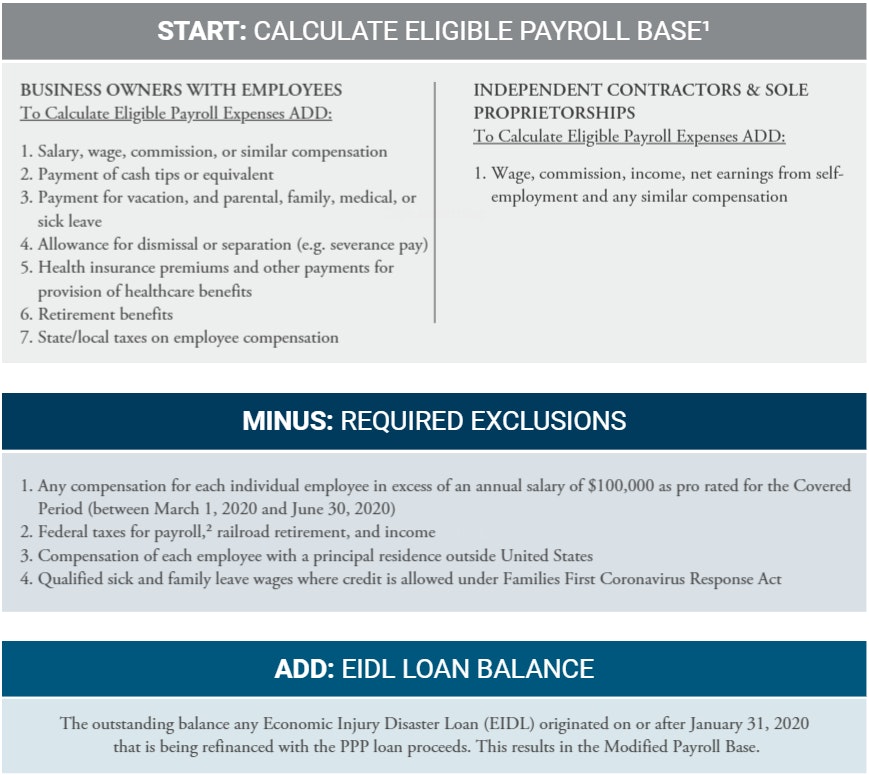

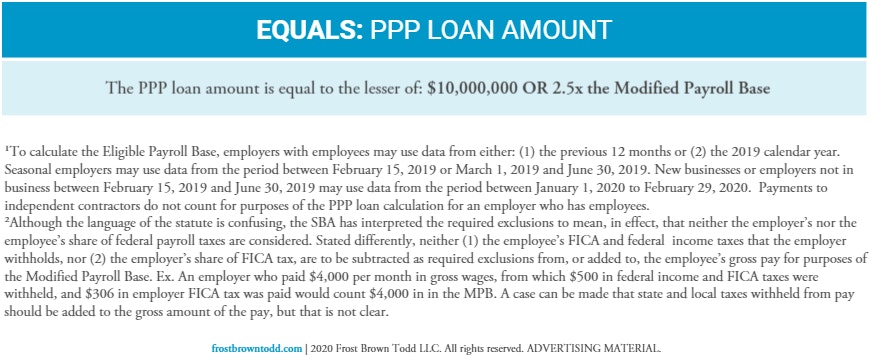

Yes, the SBA issued an Interim Final Rule detailing the requirements for independent contractors and sole proprietors. Applicants should consult Frost Brown Todd’s SBA Team and lender with questions on determining this amount as well as any other requirements specific to independent contractors and sole proprietors.Does the exclusion of employee compensation in excess of an annual salary of $100,000 apply to all employee benefits?

No, the exclusion only applies to cash compensation and not to benefits such as employer retirement contributions, health care coverage, or state and local taxes assessed on employee compensation.

Can employers use PPP loan proceeds to pay sick leave?

Yes, loan proceeds cover payroll costs, including employee vacation, parental, family, medical, and sick leave. However, the employer may not use the proceeds to cover qualified sick and family leave wages for which a credit is allowed under the Families First Coronavirus Response Act (Sec. 7001 & 7003).

Should borrowers include payments made to an independent contractor or sole proprietor in calculations of the eligible payroll costs?

A. Where the borrower makes payments to independent contractors (but the borrower is not themselves the independent contractor), the answer appears to be “No.” In the SBA’s Interim Final Rules, which were published to implement Sections 1102 and 1106 of the CARES Act, in response to the question, “Do independent contractors count as employees for purposes of PPP loan calculations?” and “Do independent contractors count as employees for purposes of PPP loan forgiveness?” the answer is the same: “No, independent contractors have the ability to apply for a PPP loan on their own so they do not count for purposes of a borrower’s PPP loan [calculation/forgiveness].” The response seems to mean that independent contractors are not to be included within the definition of “payroll costs” and should not be used to calculate either the loan amount or the amount of loan forgiveness. The response appears to contradict the definition of “payroll costs” in the text of the CARES Act, which, in general, defines payroll costs by including certain specified payments made to employees, along with certain specified payments made to independent contractors and sole proprietors. Until the SBA clarifies the Interim Rules to align them with the statute, or until it is established that the SBA cannot use the Interim Rules to contradict the statute, borrowers should consider the risks of taking independent contractors into account in calculating the loan amount or the amount of loan forgiveness and in treating payments to independent contractors and sole proprietors as an allowable use of PPP loan proceeds. Knowingly using loan proceeds for an unauthorized purpose could potentially subject the borrower to liability for fraud.

B. Where the borrower is the independent contractor, or a sole proprietor who is paid as an independent contractor, these individuals would include a an amount factored from the net profit reported on their 2019 Schedule C, in lieu of the specific payments they received, in addition to payroll costs they may have if they also employ other individuals. Applicants should consult our SBA Team and lender with questions on determining this amount as well as any other requirements specific to independent contractors and sole proprietors.

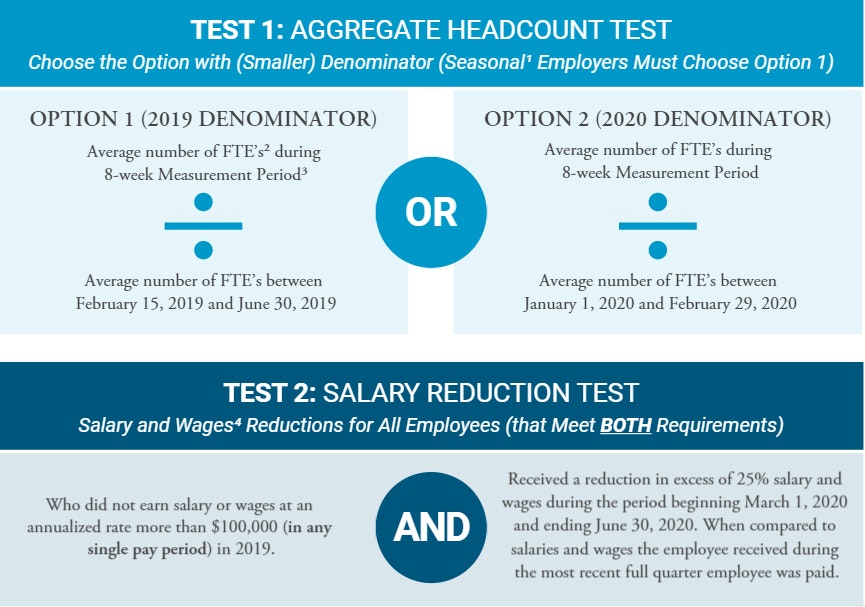

What time period should employers use to determine the number of employees and payroll costs to calculate their Eligible Payroll Base?

Most employers can calculate their aggregate payroll costs using data either from the previous 12 months or from calendar year 2019. For seasonal businesses, the applicant may use average monthly payroll for the period between February 15, 2019, or March 1, 2019, and June 30, 2019. An employer that was not in business from February 15, 2019 to June 30, 2019 may use the average monthly payroll costs for the period January 1, 2020 through February 29, 2020. Additionally, employers may use their average employment over the same time periods to determine their number of employees, for the purposes of applying an employee-based size standard. Alternatively, they may elect to use SBA’s usual calculation: the average number of employees per pay period in the 12 completed calendar months prior to the date of the loan application (or the average number of employees for each of the pay periods that the business has been operational, if it has not been operational for 12 months).

Several issues remain unresolved at this point and we are awaiting further guidance from the SBA, including:

Where one owner has a common interest in multiple affiliate entities, should the employer include the affiliate employee costs in the Eligible Payroll Base calculation where the affiliate entities are eligible to apply separately for a PPP loan?

This question is particularly important to businesses with overlapping, but differing, ownership in affiliated businesses (such as restaurant brand with different ownership at different locations when each location is owned by a different entity). For governance and accountability reasons, the affiliates with overlapping, but differing, ownership pay wish to apply separately to ensure the loan funds are not commingled.

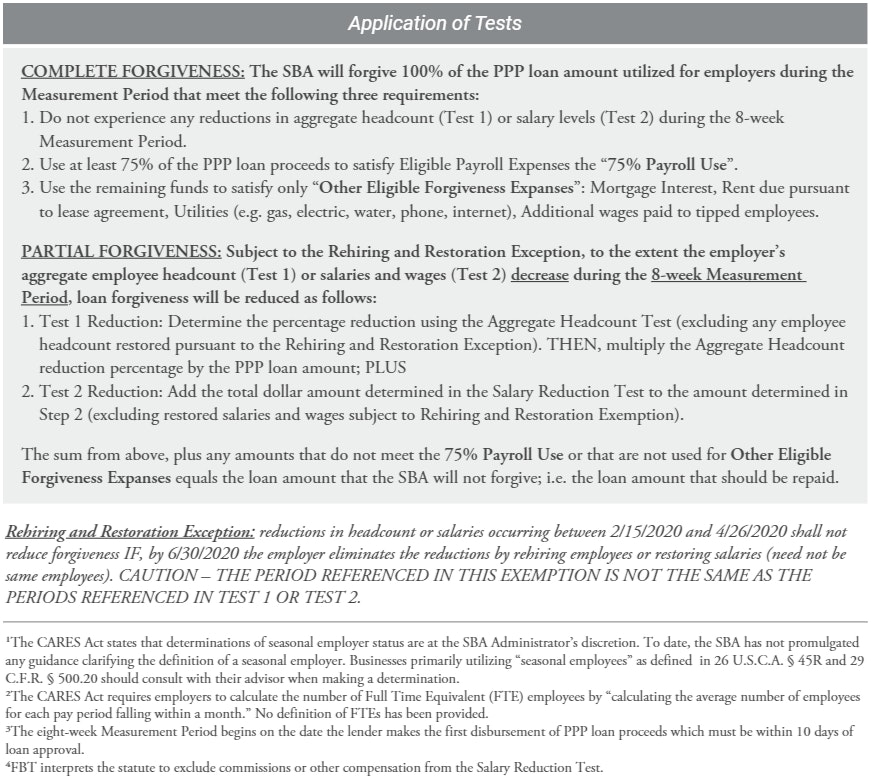

Does the Jun. 30, 2020 Rehiring and Restoration Exemption mean employers must restore the workforce in its entirety or that the amount of the loan forgiveness reduction will be proportionate to the amount of employees rehired by Jun. 30, 2020?

To eliminate a reduction in salaries and wages by Jun. 30, 2020, does an employer need to have made up the shortfall in compensation paid to employees prior to Jun. 30, 2020 or simply have restored compensation to previous levels by Jun. 30, 2020 on a going-forward basis?

Why does the Rehiring and Restoration Exemption provision use a different period than either the Aggregate Headcount Test or Salary Reduction Test? Under the exemption reference is made to rehiring employees or restoring wage reductions back to what they were at February 15, 2020.

Under the Salary Reduction Test, should employers only consider salaries and wages, or should they include commissions, benefits, and other compensation?

How are FTEs to be calculated?

The CARES Act does not specify how many hours an employee must work to be a Full Time Equivalent. While many employment related laws use differing hours to determine what constitutes a FTE (e.g., the Affordable Care Act considers 30 hours/week to constitute a FTE), the general standard is 40 hours per week although some industries or companies use a lower number of hours. Until additional guidance is received, borrowers should use the standard number of hours they traditionally seek from an employee when hiring a person as “full-time” in their calculations.

Do costs have to be both incurred and paid during the Measurement Period to be forgivable?

It is unclear whether the costs must be both incurred and paid during the Measurement Period or whether the borrower can pay costs incurred prior to the Measurement Period or prepay costs which are not due.

Can employers increase the salaries of remaining employees so that 75% of the loan is used for payroll costs to ensure their loan is fully forgiven?

There is currently no prohibition in the CARES Act or SBA guidance against increasing salaries and wages above the amounts used to determine the loan amount. However, the SBA has not affirmatively stated that this is permissible. Borrowers should also be mindful of the certification that they have to make in the application that the loan proceeds will be used to maintain rather than increase payroll.

Can borrowers pay non-mortgage interest with PPP loan proceeds?

The CARES Act permits borrowers to pay non-mortgage interest with loan proceeds but does not appear to include them as expenses eligible for loan forgiveness. Until the SBA issues additional guidance, borrowers should assume that non-mortgage interest expenses are not eligible for loan forgiveness.

*Borrowers should consult with their lender because interpretations may be different without additional SBA guidance.

[ About the Authors ]

Jeremy A. Hayden

Member Cincinnati, OH Frost Brown Todd LLC

Jeremy focuses his practice in the areas of corporate law, tax law, and estate planning. He is licensed to practice in Ohio, Kentucky, and before the U.S. Tax Court.

Jane E. Syrcle

Member Lexington, KY Frost Brown Todd LLC

Jana concentrates her practice on representing lenders in real estate and other asset based loans, construction loans, and working capital facilities and serving as bond counsel for Industrial Revenue Bonds. She also represents non-lending clients in various real estate purchase and leasing transactions and serves as opinion counsel.

Joseph W. Brammer

Associate Cincinnati, OH Frost Brown Todd LLC

Joe Brammer’s practice focuses on commercial lending and real estate. Joe will represent banks and other lenders in real estate construction and acquisition as well as asset-based and cash flow financings.

Martin E. Mooney

Member Cincinnati, OH Frost Brown Todd LLC

Marty practices in the individual and business tax areas and has extensive experience representing partnerships, limited liability companies, and corporations on issues ranging from formation to exit strategies, including reorganizations, mergers, acquisitions, redemptions, and consolidated return issues.

Rebecca M. Moore

Practice Group Leader Louisville, KY, Frost Brown Todd LLC

Becky leads the firm’s Financial Transactions Practice Group. She focuses her practice on finance and real estate transactions and has extensive experience representing lenders, borrowers, servicers, and issuers on financing transactions.